How Data Breach Insurance Protects More Than Your Network

Sep 26, 2025

The cost of a data incident is increasing year in, year out. For small and midsize businesses (SMBs), the financial damage is often too hard to absorb.

IBM’s 2025 Cost of a Data Breach Report pinned the average global cost of a breach at $4.44 million. These expenses include technical recovery, legal fees, and reputational damage.

| Danny Tehrani, CEO at Computers Made Easy, says, “Cyberattacks are hitting SMBs harder because they lack the deep pockets of larger firms.” |

This reality shows why data breach insurance is no longer optional for any business handling sensitive information. You need financial protection against events that are now almost certain, not rare.

Don’t Let a Data Incident Become a Business-Ending Event!

Implement the right cybersecurity strategies to shield your company from attacks and lower your cyber premiums.

Learn MoreWhat Is Data Breach Insurance?

Data breach insurance is a specialized policy that helps businesses manage the financial, legal, and reputational impact of data exposure. Whether the breach involves digital theft or physical loss, this coverage acts as a focused safety net for sensitive information.

Unlike general liability insurance, which covers bodily injury or property damage, data breach insurance is designed specifically for information-related incidents. It’s also more targeted than broader cyber liability insurance, which may include coverage for system outages and a wider range of cyberattacks.

Key features of data breach insurance:

- Coverage for digital & physical incidents: Protects against stolen customer data, lost devices, and exposed personal or financial information.

- Legal & regulatory support: Helps cover legal fees, regulatory fines, and compliance-related costs after a breach.

- Notification & credit monitoring services: Supports customer outreach and post-breach services like identity protection and monitoring.

- Public relations & reputation management: Assists with crisis communication to preserve brand trust and minimize reputational damage.

Whether your business stores data in the cloud or on physical devices, breaches can happen. Data breach insurance provides targeted protection for the immediate fallout, making it a vital layer in your risk management strategy.

Who Needs Insurance Against Data Breach?

Any organization that stores personal, financial, or proprietary data is at risk for data breaches and should seriously consider data breach insurance. Whether you’re a large enterprise or a small business, the consequences of a breach can be severe and costly.

However, companies that deal with more valuable data, such as medical clinics or banks, are under higher pressure to protect client and business data.

Examples of Industries Under High Pressure:

- Healthcare Providers: Must comply with HIPAA and protect sensitive patient data. Breaches can lead to fines, lawsuits, and reputational damage.

- Financial Institutions: Regulated by the SEC and FINRA, these firms handle high-value data and face strict compliance requirements.

- Legal firms: Store confidential case files and client records. A breach can compromise legal integrity and client trust.

According to Verizon’s 2019 Data Breach Investigations Report, 43% of cyberattacks targeted small and mid-sized businesses. Hackers often exploit weaker defenses, knowing these firms may lack dedicated cybersecurity resources.

Hidden costs of a breach:

- Customer notification and credit monitoring

- Legal and regulatory penalties

- Forensic investigation and recovery

- Loss of trust and business continuity

Even a modest database can become a liability without proper coverage. Data breach insurance helps absorb the financial shock, protecting your business from a crisis that could otherwise be devastating.

What Does Data Breach Insurance Cover?

Coverage usually falls into two main categories: first-party and third-party protection.

First-party coverage deals with direct costs to your business, including:

- Data Recovery and Forensic Investigation: Experts who identify what was lost, how it happened, and how to contain the issue.

- Public Relations Support: Services to protect your reputation and reassure customers.

- Customer Notification Costs: Sending legally required breach notifications to clients or patients. Each affected data record can add $150 to $200 in expenses.

- Credit Monitoring Services: Providing affected individuals with monitoring to protect against identity theft.

- Ransomware Payments: Coverage for ransom demands under certain circumstances.

Third-party coverage handles claims made against you by others. This often includes:

- Legal Defense Costs and Settlements: If customers or partners sue for damages.

- Regulatory Fines or Penalties: When agencies penalize you for non-compliance with data laws.

Real-world claims often involve both categories. For example, a dental clinic hit by ransomware may need to restore its systems (first-party) while also facing patient lawsuits over leaked health records (third-party).

Policies vary, but the takeaway is that data breach insurance covers both the cost of managing the crisis internally and the external liabilities you may face. Relying only on one type of coverage leaves dangerous gaps.

| More articles you might like: 7 Risks of BYOD & How to Avoid Them Why Cloud Security Assessments Are Important & How to Perform One Data Migration from Legacy Systems: A Step-by-Step Strategy |

Comparing Cyber Data Breach Insurance and Cyber Liability Insurance

While these two coverages often overlap, they serve distinct purposes. Choosing the right one, or both, depends on your business’s specific risks and operational priorities.

Cyber Liability Insurance

This is the broader coverage, designed to protect against operational disruptions caused by cyberattacks.

- Covers business interruption and lost revenue from downtime

- Includes protection against malware, denial-of-service attacks, and system damage

- Ideal for businesses that rely heavily on uninterrupted digital operations

Cyber Data Breach Insurance

This is more specialized, focusing on the fallout from exposed or stolen sensitive information.

- Covers costs for customer notification, credit monitoring, and forensic recovery

- Addresses reputational damage and regulatory penalties

- Best for businesses handling personal, financial, or health-related data

Why Some Businesses Need Both

A manufacturer, for example, may need cyber liability to cover production downtime, and breach insurance to protect employee payroll data. Each policy addresses a different layer of risk.

How to Decide:

- If your biggest risk is data exposure, prioritize breach-specific coverage

- If your operations depend on system uptime, consider cyber liability insurance

- For comprehensive protection, many businesses opt for both policies

What Data Breach Insurance Does Not Cover

While data breach insurance offers vital protection, it doesn’t cover every risk. Many businesses mistakenly assume it’s a catch-all solution, but exclusions are common and important to understand.

Typical exclusions include:

- Bodily Injury & Property Damage: These fall under general liability insurance, not data breach coverage.

- Employee Disputes: Claims like wrongful termination or discrimination are handled through employment practices liability insurance.

- Physical Property Loss: Damage to servers or hardware from events like floods or fires is excluded and covered under property insurance.

- Pre-existing Vulnerabilities: If security flaws were known and left unresolved before the policy began, they’re typically not covered.

Insurance is not a substitute for cybersecurity. Most providers require proof of security controls such as firewalls, encryption, and access management before issuing a policy.

If your insurer doesn’t understand your industry’s risks, you could end up with gaps in protection. Work with a provider who knows your regulatory landscape and operational needs to ensure your largest exposures are covered.

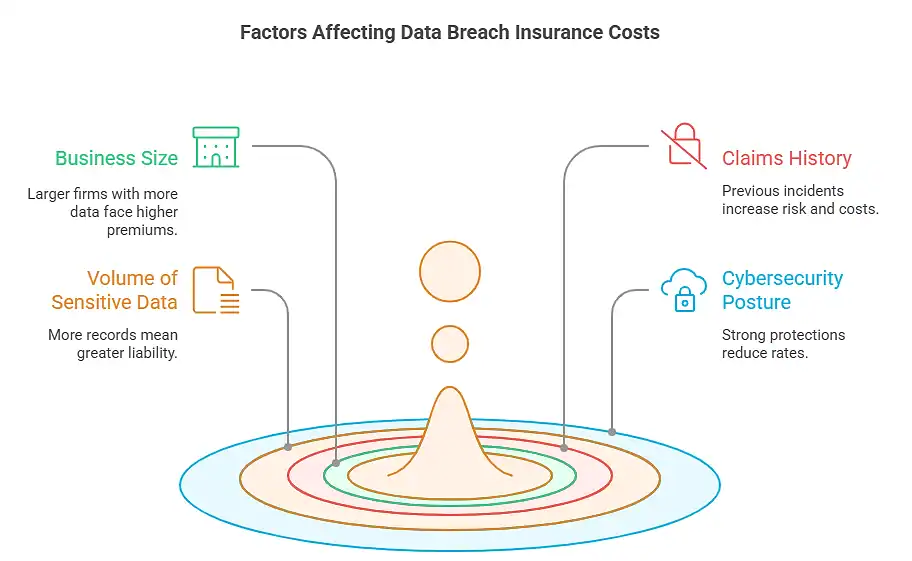

Cost of Data Breach Insurance and What Affects It

Premiums vary widely, but several consistent factors shape the cost.

- Business Size: Larger firms with more employees and data often face higher premiums.>

- Claims History: Previous incidents raise your risk profile and drive costs up.

- Volume of Sensitive Data: More records mean greater liability in the event of exposure.

- Cybersecurity Posture: Strong protections, like encryption and endpoint monitoring, can reduce your rates.

A report by Advisor Smith found that the median cost of cyber insurance for SMBs was $1,589 per year. Deductibles also vary, but businesses can often lower costs by demonstrating strong risk management practices.

Investing in cybersecurity not only reduces your exposure but can also make your premiums more manageable.

Choosing the Right Policy for Your Business

Selecting a policy requires more than comparing prices. You need to match your exposure with the right protections.

Key questions to ask providers include:

- Does the policy cover both first- and third-party costs?

- How does it define a “breach”?

- Is it a “duty to defend” policy, meaning the insurer must provide legal defense?

- What exclusions apply to my industry?

Working with providers who understand your regulatory environment is especially important. A healthcare practice needs different terms than a financial advisory firm.

The right fit ensures you do not discover dangerous gaps in coverage when it is already too late.

Practical Steps to Strengthen Coverage Value

Insurance works best as part of a larger strategy. You can increase its value by improving your internal protections.

Practical steps include:

- Employee Training: Many incidents start with phishing emails. Training reduces the chance of human error.

- Data Minimization: Store only what you truly need. Less data means less liability.

- Strong Backups and Monitoring: Quick recovery reduces the scope and cost of incidents.

- Endpoint Protection: Laptops and mobile devices are common entry points for attackers.

Framing insurance against data breach as one layer of defense helps you see it not as a silver bullet but as a financial buffer that complements prevention.

Factors That Impact Data Breach Recovery Time

Even with insurance, your recovery timeline depends on several variables. These often determine how quickly you can resume operations.

| Recovery Factor | Impact on Timeline |

| Incident response planning | Predefined steps reduce delays in decision-making. |

| Employee awareness | Trained staff report issues faster, minimizing the spread. |

| Backup availability | Regular, tested backups shorten downtime significantly. |

| Regulatory requirements | Compliance rules can extend the time needed for notifications. |

| Vendor involvement | Dependence on third parties may slow investigation and fixes. |

This table shows why pairing insurance with operational readiness creates a stronger safety net.

Lower Your Cyber Insurance Costs with Computer Made Easy’s Proven Cybersecurity Strategy

Data breach insurance is no longer a product for enterprises alone. SMBs are frequent targets and face costs they cannot afford to absorb. With the right policy, you gain financial protection against both the direct and indirect fallout of exposed data.

At Computers Made Easy, we help businesses strengthen their resilience. With over 30 years in IT and a track record of 98% customer satisfaction, our team understands the risks SMBs face daily. We guide you in aligning insurance coverage with your security strategy.

Contact us today to schedule a consultation and take the next step in protecting your business.

Contact Us

IT & Marketing Services